Take control of your finances with everything you need to create a budget that works for you and your finances. Save more and spend less with the tools you need to wipe out debt and boost your savings.

Looking for safe places to store your cash at home? Check out these secret places to keep your cash so only you can find it!

Want to learn the cheapest ways to heat your home and lower your heating costs? Read to find out how to lower your bills this winter!

Wondering how much house you can afford with a $120,000 salary? Check out this guide before purchasing your new home!

Want to learn how to afford a Lamborghini? Check out these methods to ensure you can afford a Lambo or your dream car today!

If you're looking for cheap foods to save money on your grocery bill, check out this complete list of the cheapest foods to buy!

Looking to travel on a budget? Check out these budget travel tips to spend less and travel more today!

Looking for a budgeting app that's best for you? Check out this Truebill vs Mint review to get all the answers you need!

If you want to cut back on housing costs and live affordably, check out these cheap ways to live in 2021 and beyond!

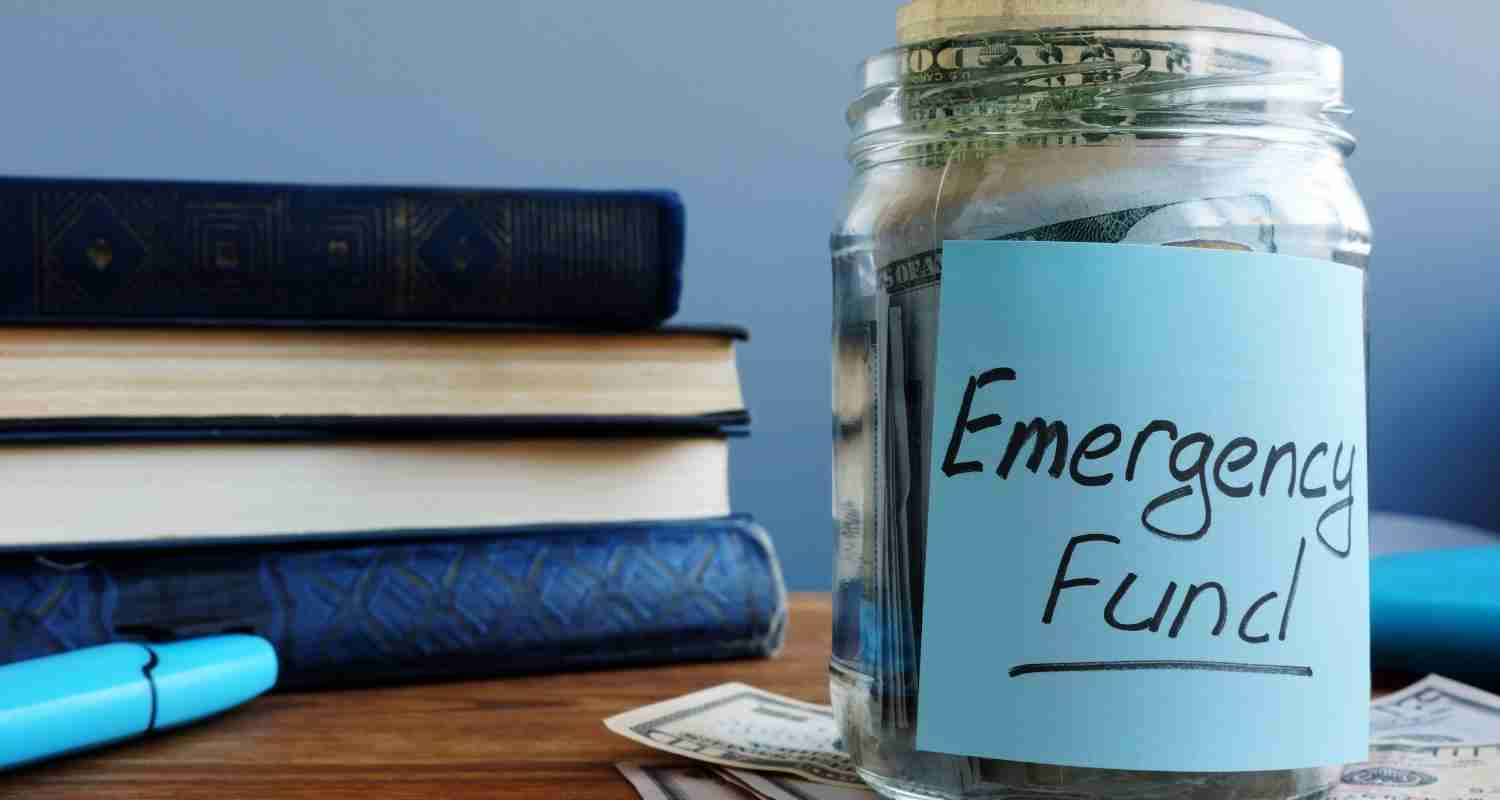

Check out these emergency fund examples to help you prepare for unexpected expenses and have money set aside for when they occur!

Want to learn how to live mortgage free? Check out these ways to live without a mortgage payment so you can save money fast!

If you're wondering "why am I broke?" and can't seem to figure out your finances, check out these reasons you could be broke!

If you need to save money fast and live frugally, check out these frugal living tips from the Great Depression.

Read to learn how much you should be spending on food, how you can save money at the grocery, and much more!

Looking to save money on your electric bill? Read to learn if using a space heater can save you money at the end of the month!